Failure Theories Abound

Silicon Valley Bank’s recent failure was capable of generating a systemic contagion that could have crippled economies worldwide. Rapid response by US regulators and monetary authorities avoided this close call, the likes of which may never have occurred in the economic history of the United States.

Fueled by rampant short selling, a plummeting stock price on the NASDAQ exchange and a full-blown bank run (some called it a “Bank Sprint”) driven into a frenzy by social media and instantaneous communication, Silicon Valley Bank spun out-of-control crashing ignominiously on an otherwise quiet Friday in early March 2023.

Financial pundits and financial know-littles had a field day with soundbites about the causes of the Bank’s failure. For example –

- The Bad Management Theory – SharkTank contestant Kevin O’Leary called the management of SVB “idiots”. It subsequently came to light that companies in which O’Leary is involved had billions deposited at the bank.

- Political Theory – Florida governor Ron DeSantis, who is expected to run for President in 2022 blamed the Bank’s failure on “WOKE politics”.

- Off-kilter Cryptocurrency advocate Cointelegraph blamed the Bank’s failure on unnamed regulators’ conspiracy to destroy Cryptocurrency.

While the theories about reasons for the Bank’s failure are uncountable, any banker will tell you “The numbers don’t lie” and the numbers at Silicon Valley Bank foretold the likely implosion of the bank several years before the bank finally failed.

The Bank Grew at Implausible Rates

Founded in 1983, Silicon Valley grew steadily over the years with its “Dedication to Entrepreneurs”. By 2016, Silicon Valley was the 44th largest bank in the US. The bank’s relatively modest growth continued through 2019, however in 2020, the Bank’s growth exploded at eye-popping rates. From 2019 to 2020, the Bank grew from the 37th largest bank to become the 29th largest in assets.

The next year, the bank vaulted over fourteen other banks to become the 15th largest bank in the US.

FDIC Call Reports chart the incredible growth of the Bank. In the 2016-2020 period, assets had grown from $44 Billion to $114 Billion. Likewise deposits lept from $79 Billion to $206 Billion.

Silicon Valley Bank’s explosive growth did not halt there. In 2021, deposits grew 86% from $206 billion to $382 Billion almost doubling in a single year.

Silicon Valley was awash with cash.

Interest Rates Made Long-Term Treasuries Look Appealing

Banks primarily invest deposits in loans. Lending is the primary function of banking. “Excess” cash is often invested in government securities usually of a very short term to avoid interest rate risk and to roughly match the maturities of the securities with expected short term cash needs.

Silicon Valley flipped this formula with catastrophic results.

United States monetary authorities had maintained near zero interest rates for a prolonged period beginning with a precipitous drop in late 2008 in response to the Banking Crisis extending into late 2021.

Interest rates reached their nadir in late 2020 when the bell weather 10 Year Treasury Note fell to .64% –

Source: Macrotrends

As long-term interest rates were falling, so were short term rates. 26 week T-Bill Coupon Equivalents yields almost vaporized, dropping to .11% during Q3 2020.

While both long and short term interest rates dropped and deposits gushed into Silicon Valley Bank, long term instruments maintained a substantially higher return than short term instruments –

Silicon Valley Bank took the bait and bought long term treasury securities rather than lend the deposits or invest in short term instruments. From 2020 to 2021, securities holdings at SVB increased at a dizzying pace while loans grew at modest rates –

Unfortunately for the Bank, interest rates, which had remained flat since early 2020, began to rise. In early 2022 in an effort to curb inflation that was running at 1970s-like rates, the Federal Reserve Bank began a series of seven rate hikes which would raise the Fed Funds Target Rate from almost zero to 4.25% – 4.5% in only nine months –

Source: Board of Governors of the Federal Reserve System

As a result, a 10-year bond purchased at par in 2020 with a 1% coupon rate for $1 million would have plummeted in value to about $800,000 two years later when yields had risen to 4.5%. Silicon Valley’s massive securities purchases were worth substantially less than face value. And depositors were now withdrawing funds at massive levels.

The Bank Run Begins

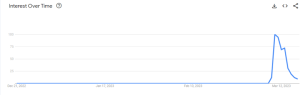

While exact withdrawal rates are not available, the press has described the bank run as being driven by social media. Using Google search results as a proxy for interest in the Bank that was translated into withdrawal action by depositors, “Silicon Valley Bank” was a sleepy search term with nominal search activity until March 8 –

On March 8 – two days before the Bank failed – searches began to surge. By the day of failure search activity was at its peak –

Sources: Google Trends

This proxy indicates that in only three days – the two days before and the day of the closing – the full-blown bank run was in progress. This conclusion is buttressed by news reports citing a single day withdrawal total at $42 Billion, leaving the Bank $1 Billion short of available cash to pay depositors.

To meet the withdrawal deluge, Silicon Valley Bank looked to their now heavily discounted long bond portfolio to meet liquidity demands. Selling at discounted prices would have effectively bankrupted the Bank. Unable to instantly raise equity, Bank management had now run face first into an insurmountable problem: Silicon Valley Bank, days before, the 16th largest bank in the United States was insolvent, had failed and required regulatory intervention to close the bank and end the bleeding.

On Friday, March 10, the California Department of Financial Protection and Innovation closed the Bank and appointed the Federal Deposit Insurance Corporation as the Receiver for Silicon Valley Bank.

Conclusion

What should Silicon Valley Bank have done to better manage the interest rate risk that eventually caused its failure?

Was the Bank’s failure inevitable?

What could Silicon Valley done to manage interest rate risk?

See our next post “THE SILICON VALLEY BANK SAGA PART 2: THREE WAYS TO DEAL WITH INTEREST RATE RISK”

Talk to BankLabs 501.246.5148 or sales@banklabs.com to discuss how we can help you manage participations and interest rate risk.