If you’re a banker trying to keep lenders lending while managing concentration risk, liquidity pressure, and staffing constraints, you’ve probably bumped into the same bottleneck: the “capital markets” tools you need (loan participations, loan sales, syndications) are often run on spreadsheets, email, and manual reconciliation.

That works—until it doesn’t. As volumes rise, portfolios diversify, or participants expand, the operational drag and “out-of-balance” risk climb fast. And when the process is heavy, the business outcome is predictable: fewer sell-downs, fewer partners, slower closings, and missed opportunities.

This guide breaks down how loan participation (plus syndications and whole-loan sales) actually work, why they matter right now, and what a modern bank should look for if you’re evaluating tools to do this at scale.

Key takeaways

-

Loan participation lets you share a single loan’s exposure while keeping the borrower relationship with the lead lender—great for lending limits, concentration risk, and liquidity planning.

-

Loan syndication typically forms a lender group at origination under a common structure—useful for larger deals and shared underwriting at close.

-

Whole-loan sales transfer the entire loan to another party—often used for liquidity, balance sheet repositioning, or portfolio strategy.

-

Regulators expect buyers to underwrite and administer purchased loans/participations as if originated by the buyer—and caution against over-reliance on sellers.

-

The banks that win here treat participations as a repeatable operating system, not a one-off legal project.

Want a faster, safer way to run loan participations and loan sales? Explore how Participate (a BankLabs innovation) helps banks automate workflows, participant servicing, and reporting—without living in spreadsheets.

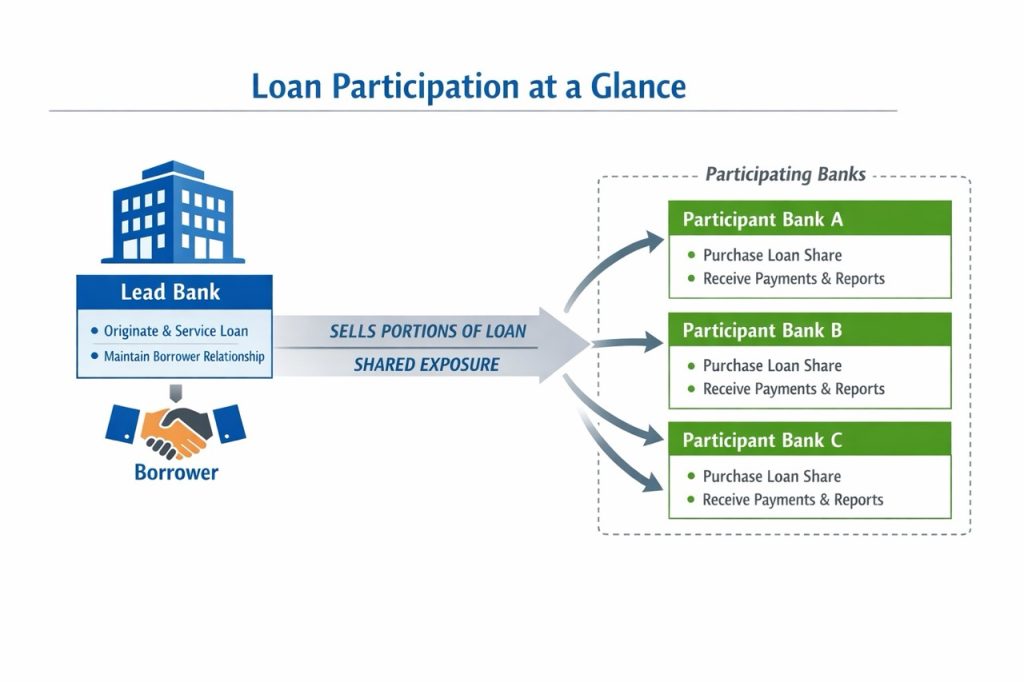

Loan participation structure showing lead bank, participants, and shared exposure while the lead retains borrower relationship.

What is a loan participation?

A loan participation is when the originating (lead) bank sells a portion of a loan to one or more participating institutions, while typically retaining the borrower relationship and servicing role.

Why banks use loan participations

Most banks use loan participations to:

-

Stay within legal lending limits while keeping the client relationship

-

Reduce concentration risk (borrower, industry, geography, tenor)

-

Improve liquidity flexibility by selling down exposure

-

Generate fee income via servicing/administration in many structures

-

Build reciprocal partner networks (send deals, receive deals)

Loan participation vs. “just buying a loan”

From a workflow standpoint, participations can look like “loan buying,” but they introduce ongoing operational complexity:

-

Shared balances must remain aligned

-

Payments/fees/rate changes need accurate allocation

-

Reporting and notices go to multiple institutions

-

Documents must be controlled and auditable

Expert tip: If your team says “we reconcile it at month-end,” you’re carrying unnecessary operational and reputational risk—because participant confidence erodes long before month-end.

Loan participation vs. loan syndication vs. whole-loan sale

Here’s a practical way to choose the right structure.

1) Loan participation (most common for many community/regional use cases)

Best when you want to:

-

Keep the borrower relationship

-

Sell down exposure post-close or near-close

-

Work with a small group of known partner banks

-

Maintain speed and flexibility

2) Loan syndication (common for larger, structured deals)

Best when you need:

-

Multiple lenders committed at origination

-

A clearer “agent/arranger” structure

-

Formal coordination across the lender group

-

Standardized communications and consent mechanics

3) Whole-loan sale (clean transfer)

Best when:

-

You want full liquidity relief

-

You’re repositioning a portfolio

-

A buyer wants full ownership/control

-

You want to simplify ongoing administration (because you no longer service)

Why loan participations matter more right now (and what regulators are signaling)

Balance sheets have been under pressure: liquidity planning, credit normalization, and concentration scrutiny are not theoretical—they’re daily management issues.

Regulators have been explicit that when institutions purchase loans or participations, they should manage them with the same rigor as originated assets and avoid over-reliance on lead institutions or third parties.

The OCC similarly frames loan purchase activities (including participations and participations in syndicated loans) as long-standing practices that must align with strategy, risk appetite, and strong due diligence/credit administration.

Did you know? The FDIC updated its advisory (amended February 3, 2026) to remove references to reputation risk—while keeping the core expectations around independent underwriting, administration, and third-party risk.

The real bottleneck: operations, not opportunity

Most banks don’t struggle with why to do participations—they struggle with how to do them repeatedly without friction.

Common pain points in traditional loan participation workflows

-

Manual “system of truth” issues (multiple spreadsheets, versions, email chains)

-

Out-of-balance risk between lead and participants

-

Slow participant communications (rate changes, payments, remittance notices)

-

Document sprawl (attachments, unsecured sharing, scattered files)

-

Limited visibility for leadership (portfolio analytics, performance reporting)

-

Scaling constraints (volume increases require headcount increases)

This is exactly why automated platforms are showing up in bank operating models: not to “innovate for innovation’s sake,” but to make participation activity repeatable and auditable.

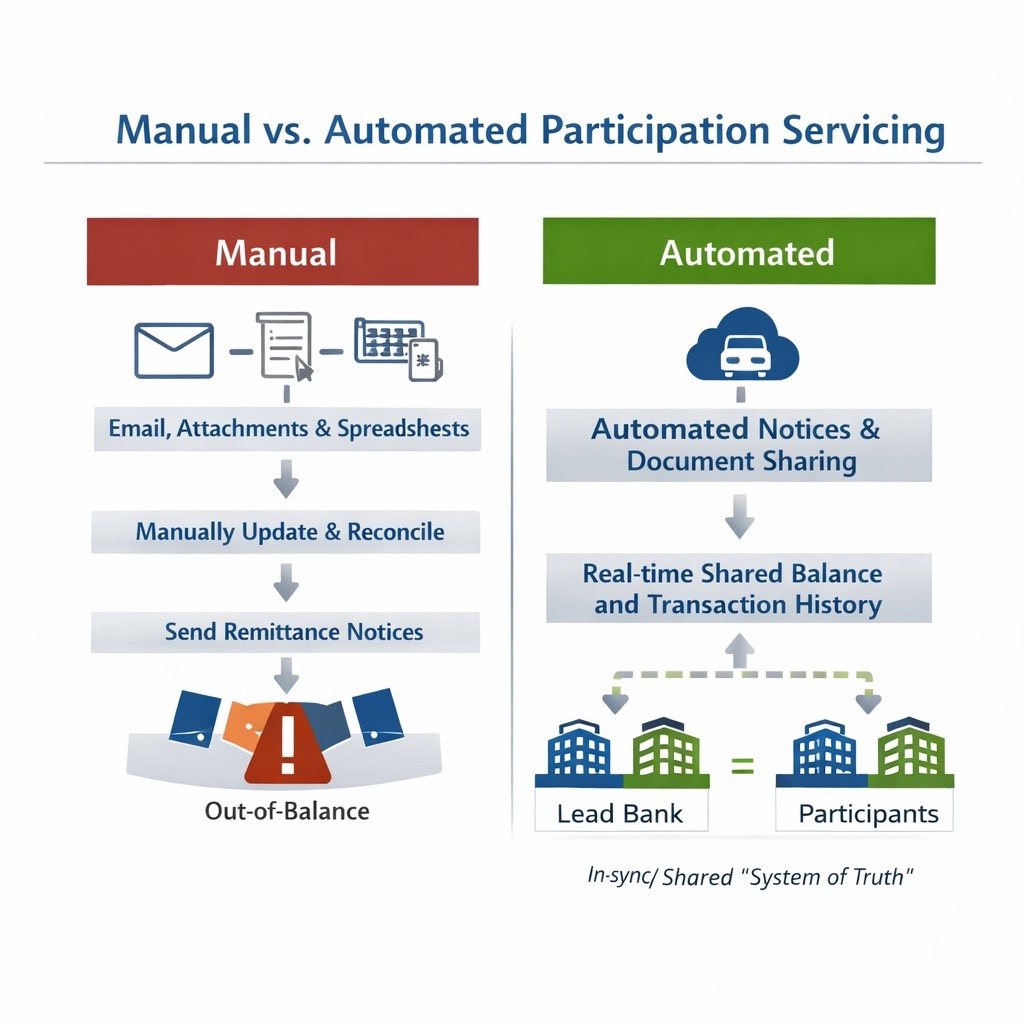

Side-by-side workflow comparing spreadsheet/email processes to automated servicing with real-time balances and automated notices.

What “loan participation automation” actually means

When bankers hear “automation,” they sometimes imagine a rip-and-replace, loan participation automation actually means:

A) A standardized workflow for selling down and onboarding participants

-

Publish the opportunity (internally or to approved partners)

-

Secure document sharing + approvals

-

Built-in NDAs/participation agreement workflow (or your own templates)

-

Track status and commitments

B) Ongoing participant servicing without manual reconciliation

-

Automated payment splits (principal/interest/fees)

-

Automated rate change notices

-

Shared balances and transaction history

-

Centralized documents + audit trail

C) Reporting and visibility that helps you scale

-

Buy-side / sell-side dashboards

-

Portfolio analytics

-

Board-friendly reporting

-

Exception-based operations rather than “touch everything”

Expert tip: Ask vendors one blunt question: “Who is the system of truth when our core and our participants disagree?” The best answers include shared balances + traceable transaction history.

A buyer-centric checklist: what to look for in a loan participation tool

If you’re evaluating solutions (or even building internally), here’s a practical checklist.

Workflow + speed

-

Can you package and share an opportunity in minutes, not days?

-

Can you control distribution (specific partners vs. broader network)?

-

Can you track approvals and commitments without chasing email?

Servicing + controls

-

Do participants see the same balance and history you see?

-

Are rate changes and notices automated?

-

Is reconciliation built into the process (or offloaded to month-end)?

Data + integrations

-

Can it integrate with your LOS/core (or start quickly without deep integration)?

-

Does it support the data elements you care about (loan terms, covenants, reporting)?

-

Can you onboard existing participations to get value immediately?

Risk + compliance alignment

-

Secure document handling and permissioning

-

Audit trail and approvals

-

Clear third-party risk management support (SOC posture, access controls, etc.)

Where Participate fits

Loan participations and loan sales are powerful tools — but without the right operating structure, they become operationally heavy.

As participation volume grows, spreadsheets, manual notices, and reconciliation work can limit scalability. What starts as a strategic advantage can quickly turn into administrative drag.

Participate, developed by BankLabs, is built to serve as the operating layer for loan participations, syndications, and loan sales. It standardizes workflow, automates participant servicing, and creates real-time balance transparency between originators and participants.

With the right system in place, banks can:

-

Automate deal workflow and participant onboarding

-

Maintain real-time shared balances

-

Eliminate reconciliation friction

-

Centralize documentation and reporting

-

Scale participation activity without scaling headcount

The outcome is simple: more confidence, less operational risk, and a repeatable framework for growing your loan sales ecosystem.

FAQ

What is the difference between a loan participation and a loan syndication?

A loan participation typically involves a lead lender selling portions of a loan (often after origination) while keeping the borrower relationship. A syndication usually forms a lender group at origination under a coordinated structure (often with an agent/arranger).

Can smaller banks benefit from loan participations?

Yes. Participations allow smaller institutions to access larger deals, diversify portfolios, and manage exposure more effectively.

How do loan participations help with concentration risk?

They let you sell down exposure by borrower/industry/geography/tenor while keeping the client relationship and continuing to originate new business.

What’s the biggest operational risk in participations?

“Out-of-balance” conditions and incomplete information sharing—especially around payments, rate changes, fees, and document versions. That risk grows with volume and participant count.

Can we modernize without a massive integration project?

Yes, with Participate you can go live in less than 24 hours. Many banks start by standardizing workflow and servicing visibility first, then expand integrations over time based on ROI and operational readiness.

Conclusion

Loan participations, syndications, and loan sales aren’t niche tools—they’re core levers for balance sheet strategy, risk management, and growth. The difference between “we do participations occasionally” and “we do participations confidently” is almost always the operating model: visibility, controls, and repeatability.

If you want to turn loan participation activity into a scalable process—without adding headcount or living in reconciliation—explore Participate’s approach to workflow + servicing automation. Request a Free Demo.